I hardly ever write about personal finance, even though I am very interested and reasonably well read in it, being retired. But a recent article in the Wall Street Journal (free link)about QLACs, or Qualified Lifetime Annuity Contracts, started me thinking.

Millions of Americans have good reason to worry they will outlive their retirement savings. A little known tax-advantaged annuity can help avoid that, providing a guaranteed income in the final years of life.

Starting this year, Americans can use up to $200,000 of their retirement accounts to purchase qualified longevity annuity contracts, or QLACs. ...

An annuity is an insurance contract that you can buy to provide a steady income like a pension, making it easier to plan for the uncertainty of life expectancy. QLACs have existed for a decade and offer significantly more income for life than a typical immediate annuity, since the payments don’t start until later in life, at, say, age 80 or 85. They also have a special tax benefit.

The shift from the security of pensions to relying on 401(k)s turned workers into both investors and actuaries, tasked with building a nest egg big enough to last their lifespan. QLACs are a way to remove some of that guesswork.

Let me be clear: I have no annuities now and no intention of ever getting one. My father was an agent for one the country's largest life insurance companies. Starting near the end of his career, the company began selling brokerage products, including annuities, in addition to insurance. One day I was home visiting and he took me to a seminar at his office on annuities (we were going to the golf course afterward). Everything I heard there convinced me never to buy one.

The WSJ's article on QLACs made me wonder whether there is a way for individual investors like me to guarantee lifetime income the way that QLACs do, but without simply handing up to $200,000 over the the annuity company, locking it up:

The drawbacks to a QLAC are the upfront cost and that if an emergency occurs and you need money before the beginning of payouts, you can’t touch it. It is locked in. The size of the payout also depends on how long you live.

My wife is 65. I have promised our kids that I will provide for her until she turns 100, but then she is their problem. This is a very realistic expectation since she comes from a family of Methuselahs, of whom living to very late 90s and beyond is quite common.

So I thought, how to take, say, a QLAC's $200,000 and self annuitize it until 2058? The first thing I tried was to withdraw annually an amount of money equal to the balance on hand divided by the number of years left to go. And bingo! It worked. So the first year's withdrawal would be $200,000 / 35 = $5,714. And I let Excel do the rest:

High-yield savings accounts stand out from traditional savings accounts in that they reward you with a higher interest rate, allowing your money to grow even faster as it sits in your account.It’s important to note, however, that the APY that savings accounts offer when you sign up can change at any time. These rates are variable and often go up or down in accordance with the Federal Reserve changing its benchmark interest rate.Not only does your money earn a better return in a high-yield savings account, but you still have access to your cash when you need it as you would in a normal savings account. Your money in a high-yield savings account should be federally insured by the Federal Deposit Insurance Corporation (FDIC), which means that deposits up to $250,000 are protected if the bank were to suddenly collapse.

1. The share price of the equity increases over time, so your invested principal increases in value with no further action by you.2. The dividend paid also increases over time, usually per year, so that the amount of dividends paid per share also increases.

- SPY, with 10-Year Average Annualized Return, 12.30%

- IVV, 12.28%

- VOO, 12.35%

- SPLG, 12.27%

- IVW, 13.79

- RSP, 10.71

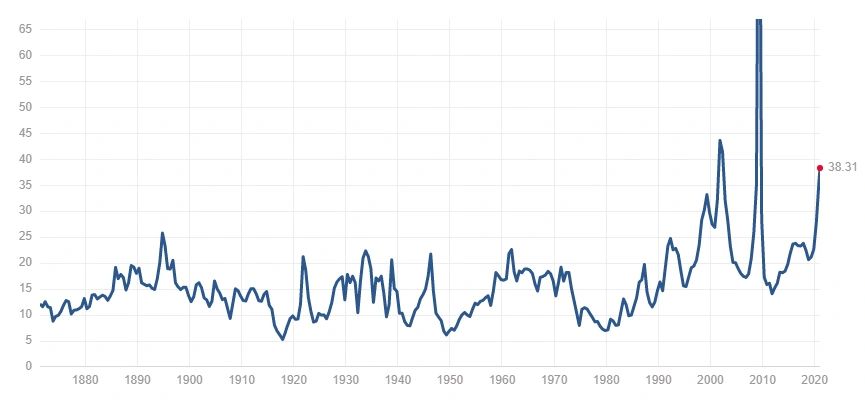

With withdrawals increasing an average of 12.28 percent per year, you will beat the tar out of inflation. But (and there is always a "but," right?), "annual average" does not mean "every year." Here is the chart of high earner IVW over the last five years.

So, it's return is neither a uniform nor guaranteed. That needs to be considered for self annuitizing for life, too. This chart, however, reflects only share price. Here is the chart with dividends included:

It is very important to assess your comfort level relative to risk of loss compared to likelihood of gains.

Conclusion

I think I have demonstrated that it is possible to self annuitize for life. To start with an expected longevity age, the IRS publishes Publication 590-B because that is what they use to determine Required Minimum Distributions (RMDs) from IRAs and other taxable retirement accounts. The IRS updates the pub intermittently, the latest table is here.

Be aware also that the figures of my worksheet may be overridden by RMDs if you include taxable accounts. If the calculated withdrawal is less than the RMD for that year, then you must withdraw more money to equal the RMD (or more, if you want).

But being required to withdraw at least the RMD does not mean you have to spend it. You can transfer all or part of it to ordinary investment or banking accounts and continue to use them for self annuity balances, or anything else.

My wife and I are both retired now. We do not intend to self annuitize as I have described, however, because we do not need to. We withdraw what we need to and leave the rest in various equities and accounts as described above. But we also know the day may come when self annuitizing those accounts will be the best solution once we reach our truly elderly years.

And that is one of the major beauties of self annuitizing - you never tie your money up handing it off to some corporation. It is always yours and you can begin self annuitizing it when you want or need to. No matter when you start, the calcs always guarantee a lifetime income.

Good luck!

End notes:

WSJ, free link: You May Need Less Money Than You Think for Retirement

For the record, I am not a financial advisor. Nothing I write here is intended to be actual advice, just some things to think about. I sell no products of any kind related to finance. In fact, I sell no products of any kind period. Did I mention that I am retired?

Here are a few more dividend leaders for 2023 so far:

- GSL, Global Ship Lease, Inc., Year To Date Return, 34.92%

- OBDC, Blue Owl Capital Corporation, 26.76%

- JEPQ, JPMorgan Nasdaq Equity Premium Income ETF, 25.79%

- EOI, Eaton Vance Enhanced Equity Income Fund, 16.81%

- AMLP, Alerian MLP ETF, 15.56% (MLP means Master Limited Partnership)

- MLPA, Global X MLP ETF, 13.32%

- AOD, Aberdeen Total Dynamic Dividend Fund, 11.59%

- JEPI, JPMorgan Equity Premium Income ETF, 6.46%

- ARLP, Alliance Resource Partners, L.P., 7.41%